Posted on Thursday, October 14 2010 @ 18:39 CEST by Thomas De Maesschalck

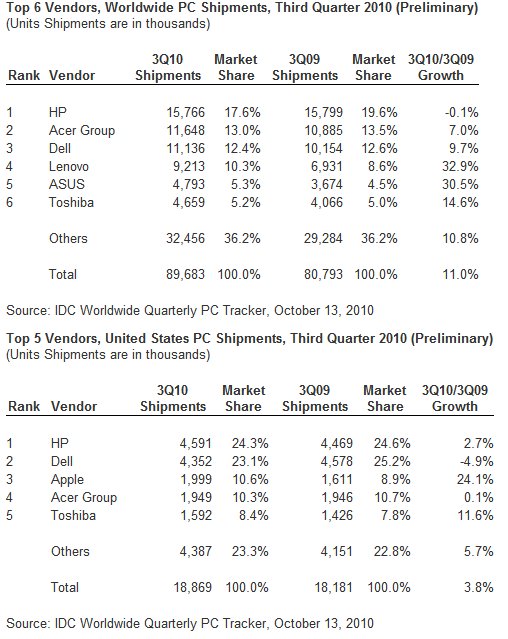

IDC released a report about PC shipments in the third quarter of this year. One of the interesting conclusions is that Apple is now the third biggest computer vendor in the US, behind Dell and HP, with a marketshare of 10.6 percent thanks to a 24.1 percent year-over-year growth in shipments. Worldwide HP is the largest PC vendor with a marketshare of 17.6 percent, followed by Acer at 13.0 percent and Dell at 12.4 percent.

The global PC market grew 11% in the third quarter of 2010 (3Q10), nearly 3% below expectations. According to the International Data Corporation (IDC) Worldwide Quarterly PC Tracker, constrained consumer spending resulted in a tepid back-to-school season but commercial refresh remained largely on schedule and the overall market improved in September compared to the earlier part of the quarter. Moreover, the market still exhibited positive sequential growth over the second quarter which is the hallmark of third quarter activity. Shipments for most markets were relatively close to expectations, with Japan surpassing the forecast. The U.S. saw the largest difference with forecast growth, coming in at a 3.8% year-on-year increase, which was well below 2Q10 growth of 11.7% and 3Q10 projections near 11%.

“Despite a sluggish start, the quarter ended with a good rally in September which could be a good prelude for what is ahead”

Continuing from trends seen in recent quarters, Desktop volume was supported by commercial purchases while consumer fatigue was evident on the Notebook side, with Mininotebook PC shipments continuing the recent trend of slowing growth.

"Despite a sluggish start, the quarter ended with a good rally in September which could be a good prelude for what is ahead," said Jay Chou, research analyst with IDC's Worldwide PC Tracker Program. "Lower PC component costs, budding excitement around new media-centric form factors and continued business buying should still make for a competitive holiday season.”

"Apple's influence on the PC market continues to grow, particularly in the U.S., as the company's iPad has had some negative impact on the mininotebook market. But, the halo effect of the device also helped propel Mac sales and moved the company into the number three position in the U.S. market," said Bob O'Donnell, IDC vice president for Clients and Displays.

Regional Outlook

* United States – Weak back-to-school sales and consumer fatigue characterized the market. The region grew 3.8% compared to a year ago, 7% below forecast, but still managed to record a positive sequential growth compared to the second quarter of 2010.

* Europe, Middle East and Africa (EMEA) – As expected maintained healthy double-digit growth in the back-to-school period, driven by continued recovery across the emerging markets and increasing business renewals in Western Europe. However, mininotebook demand continued to drop as anticipated leading to softer consumer growth.

* Japan – This was the only region to exceed forecast. Stronger than expected activity in the enterprise and SMB sector helped propel the market.

* Asia/Pacific (excluding Japan) – The region came in about 2% below projections at 13% yearly growth, as retail inventory in China and Indonesia impacted notebooks there. Desktops were slightly stronger than expected, but it was not enough to completely offset notebooks.

Vendor Outlook

* HP had a flat year overall but and managed to grow almost 3% in the U.S. Channel issues in Asia/Pacific were a contributing factor.

* Acer Group saw inventory issues cause backlog in the channel. Acer grew slightly slower than the market – primarily a result of strong year-ago performance. This was most evident in the United States and Japan, which saw the slowest growth. Meanwhile, Acer continued to make rapid gains in emerging markets.

* Dell grew nearly 10% overall and its business in emerging markets remains robust.

* Lenovo was strong across the board and gained more than 30%. Its Desktop sales benefited from continued business renewal projects and held on to have impressive gains in all regions, including its home turf in Asia/Pacific.

* ASUS continued to make strong gains across most regions despite having some inventory issues. Strong performance in Asia/Pacific helped it achieve growth of more than 30%.

* Toshiba grew

above market and saw shipments increase more than 14% for the quarter as its notebooks continued to find good reception in the Asia/Pacific (excl. Japan) region. The company also saw solid growth in the U.S. and EMEA as well.