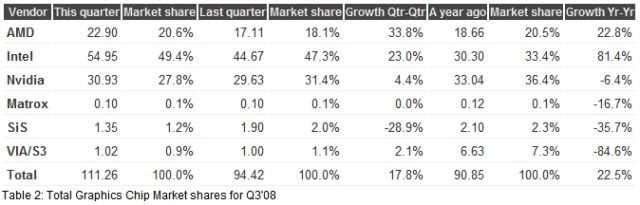

Despite the crisis on the financial markets, the graphics market saw its biggest increase in third-quarter shipments in six years. Thanks to its dominance in the IGP chipset market, Intel remains the biggest player with a marketshare of 49.4 percent, significantly up from 33.4 percent in the third quarter a year earlier. Despite a shipments growth of 22.8 percent year-over-year, AMD's marketshare in the GPU market remained flat. A year ago the firm held 20.5 percent of the market and last quarter it was 20.6 percent. NVIDIA on the other hand lost marketshare, it's shipments faced an annual loss of 6.4 percent, and its marketshare dropped from 36.4 percent a year ago to 27.8 percent in the third quarter. However, NVIDIA's GPU unit shipments were still 4.4 percent higher than in the second quarter of this year.

In the desktop market, Intel increased its first place position to 43.9 percent, while NVIDIA slipped to 32.6 percent and AMD climbed up to 20.3 percent. In the notebook GPU market, Intel held a marketshare of 56.2 percent, down 0.9 percent over last quarter, while NVIDIA declined to 21.8 percent and AMD jumped to 20.9 percent.

Desktop GPU shipments saw an increase of 4.7 percent this quarter to 61.9 million units, while notebook GPUs soared by almost 40 percent to 49.4 million units.

"The third quarter is seasonally up as OEMs place orders for chips to build inventory for the holiday season. However, this quarter was up more than any other for some time, and in spite of suggestions of a recession that started last Q4," said Dr. Jon Peddie, president of Jon Peddie Research in Tiburon California. "Desktops increased seasonally and notebooks enjoyed quite significant gains."

Peddie notes that Q4'08 will be an interesting quarter as AMD and Nvidia are not expected to release any more new GPUs given the large number of introductions in the last three quarters, and Intel and AMD have stabilized on their integrated offerings.

Further, says Peddie, although there was amazing growth in Q3 this year, the gloom and doom scenarios are having their effect on business and consumer spending plans, and while Q4 is usually the crescendo of the year, it could well be flat (compared to Q3) this year.