The report does not contain specific marketshare data for the discrete graphics card market, but it shows Intel gaining at the expensive of AMD and NVIDIA.

Jon Peddie Research (JPR), the industry's research and consulting firm for graphics and multimedia, announced estimated graphics chip shipments and suppliers' market share for Q4'12.

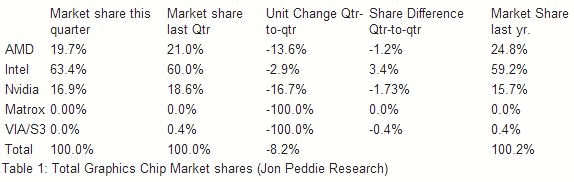

The news was disappointing for every one of the major players. AMD dropped 13.6%, Intel slipped the least, just 2.9%, and Nvidia declined the most with 16.7% quarter-to-quarter change, this coming on the heels of a spectacular third quarter. The overall PC market actually grew 2.8% quarter-to-quarter while the graphics market declined 8.2% reflecting a decline in double-attach. That may be attributed to Intel's improved embedded graphics, finally making "good enough" a true statement.

On a year-to-year basis we found that total graphics shipments during Q4'12 dropped 11.5% as compared to PCs which declined by 5.6% overall. GPUs are traditionally a leading indicator of the market, since a GPU goes into every system before it is shipped and most of the PC vendors are guiding down for Q1'13.

The turmoil in the PC market has caused us to modify our forecast since the last report; it is less aggressive on both desktops and notebooks. The popularity of tablets and the persistent recession are the contributing factors that have altered the nature of the PC market. Nonetheless, the CAGR for PC graphics from 2012 to 2016 is 3.2%, and we expect the total shipments of graphics chips in 2016 to be 549 million units.

The ten-year average change for graphics shipments for quarter-to-quarter is a growth of -1.3%. This quarter is below the average with an 8.2% decrease.

Our findings include discrete and integrated graphics (CPU and chipset) for Desktops, Notebooks (and Netbooks), and PC-based commercial (i.e., POS) and industrial/scientific and embedded. This report does not include handhelds (i.e., mobile phones), x86 Servers or ARM-based Tablets (i.e. iPad and Android-based Tablets), Smartbooks, or ARM-based Servers. It does include x86-based tablet

The quarter in general

AMD's quarter-to-quarter total shipments of desktop heterogeneous GPU/CPUs, i.e., APUs increased 0.8% from Q3 and declined 19.1% in notebooks. The company's overall PC graphics shipments slipped 13.6%. Intel's quarter-to-quarter desktop processor-graphics EPG shipments increased from last quarter by 3%, and Notebooks fell by 6.76%. The company's overall PC graphics shipments dropped 2.9%. Nvidia's quarter-to-quarter desktop discrete shipments fell 15.1% from last quarter; and, the company's mobile discrete shipments dropped 18.4%. The company's overall PC graphics shipments declined 16.7%. Year to year this quarter AMD shipments declined 29.4%, Intel dropped 5%, Nvidia slipped 4.6%, and VIA fell 10% from last year. Total discrete GPUs (desktop and notebook) 15.9% from the last quarter and were down 9.7% from last year for the same quarter due to the same problems plaguing the overall PC industry. Overall the trend for discrete GPUs is up with a CAGR to 2016 of 3.2%.

Ninety nine percent of Intel's non-server processors have graphics, and over 67% of AMD's non-server processors contain integrated graphics; AMD still ships IGPs.

Year to year for the quarter the graphics market decreased. Shipments were down 3 million units from the same quarter last year.

Graphics chips (GPUs) and chips with graphics (IGPs, APUs, and EPGs) are a leading indicator for the PC market. At least one and often two GPUs are present in every PC shipped. It can take the form of a discrete chip, a GPU integrated in the chipset or embedded in the CPU. The average has grown from 1.2 GPUs per PC in 2001 to almost 1.4 GPUs per PC.