Most of it going to advanced nodes

EE Times writes the bulk of the capex is going to cutting-edge nodes.TSMC said during a conference call with analysts that it upgraded the target in order to meet increasing demand for advanced and specialty technologies in the next several years. About 80% of the budget will go to leading process technologies, including 3nm, 5nm and 7nm, with the remaining 10% earmarked for advanced packaging and mask making, and about 10% for specialty technologies.Over the next three years, TSMC expects to invest about $100 billion to increase production capacity and boost R&D.

“We are witnessing a structural increase in underlying semiconductor demand as a multi-year megatrend of 5G and HPC (high-performance computing)-related applications are expected to fuel strong demand for our advanced technologies in the next several years,” TSMC CEO C.C. Wei said on the call. “Covid-19 has also fundamentally accelerated the digital transformation, making semiconductors more pervasive and essential in people’s lives.”

4nm and 3nm in 2022

TSMC said its 4nm process, a refined version of its 5nm node, will hit volume production in 2022. The first commercial production on 3nm is expected in the second half of 2022.Fab tools are skyrocketing

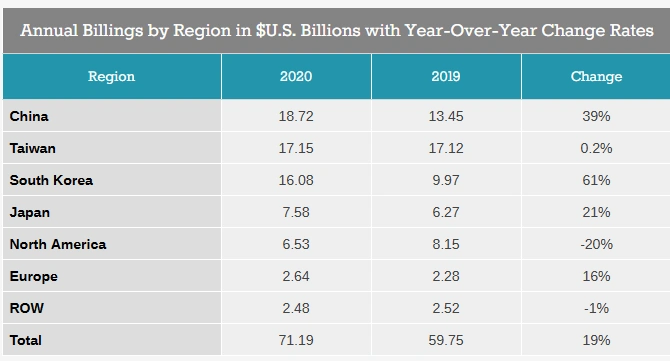

In related news, AnandTech has an interesting overview about fab tool sales. These are the tools that are used by semiconductor foundries and chip makers. Sales of semiconductor production equipment hit an all-time record of $71.19 billion last year, up 19 percent year-over-year.It's probably no surprise that Asian countries are buying up most fab tools -- not only due to the presence of TSMC in Taiwan and Samsung in South Korea, but also because of China's drive to become more self-reliant in terms of semiconductor production.

One interesting line in here is that despite the boom in semiconductor fab tool sales, the US is falling behind. Europe did buy a bit more fab tools -- but its share of the pie is very small, even compared to the US. If the US and Europe want to become bigger players in the global semiconductor market, a lot more investment will be needed to jumpstart domestic production.

Meanwhile, tool purchases by American fabs actually dropped by 20% versus the previous year, sinking to $6.53 billion for 2020. The US is still the runaway leader for chip design, so the drop serves to widen the gap between how much is designed in the country versus how little is fabbed there. Overall it looks like the tables are going to turn in the coming years as Intel, Samsung Foundry, and TSMC begin to equip their new fabs in the USA; but for now, fab tool shipments are down significantly.